The Business Context

A residential PropTech’s business model depended on accurate property valuations at every stage of its pipeline. Marketing used valuations to qualify inbound leads worth purchasing. Sales used them to construct offers to prospective clients. Finance used them to underwrite assets and report portfolio value to lending partners.

Despite the reliance on valuations, each department was utilizing a different data resource. Marketing was running on Melissa Data. Sales was producing offers against RPR's RVM product. Finance was carrying forward whichever figure arrived with the deal. This did not happen by design, but instead was the product of each department solving its own immediate problems with whatever tools were available. However, this produced an ongoing and compounding issue across departments. The client marketing qualified, the offer sales made, and the value finance was underwriting against were routinely different figures on the same property. The inconsistency was silent, systematic, and compounding at every stage of the pipeline.

In addition to the data quality problem was a cost structure problem that was quickly escalating. The business was running over $20,000 per month across three vendors, DataTree AVM, Attom Mortgage API, and Melissa, all priced on a per-API-call model. As the business expanded from 3 markets toward 33 states, that cost would scale proportionately with volume. There was no ceiling. Every new market, every new agent, every new lead purchased added to the monthly data bill.

The business needed a unified valuation source across all departments. It also needed a cost structure that wouldn't grow linearly.

My Role

I identified both problems, built the analytical case for consolidation over several months, managed the vendor evaluation and negotiation process, secured executive buy-in, and defined the infrastructure architecture for the replacement system. I also coordinated the accuracy validation with our senior analyst before making the final recommendation to leadership.

This was not exactly straightforward because it required navigating contract timing windows, a vendor attempting to renegotiate previously agreed pricing, a DataTree billing error that introduced additional commercial complexity, and the need to validate a replacement AVM product against real transaction data in order to build confidence for our investors and lending partners.

Identifying the opportunity

The consolidation opportunity emerged when our Attom contract came up for renegotiation. Attom was already providing mortgage and deed data via API as a supplement to existing resources. I inquired about the possibility of bundling nationwide bulk assessor data plus their proprietary AVM product. This arrangement would replace multiple vendor relationships at a significantly lower total cost. A 90-day cancellation window created real urgency, and missing it meant locking in at a higher monthly rate for three years with no exit.

Validating the Replacement AVM

Before recommending any transition I ran an independent accuracy analysis comparing Attom AVM against RVM across 1,400+ offers from a recent 45-day period. I followed this with a broader multi-state validation to ensure Florida results held nationally.

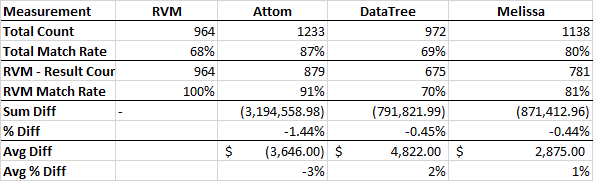

AVM Accuracy Comparison — Four Vendor Analysis

Comparative accuracy analysis across RVM, Attom, DataTree, and Melissa. Attom AVM shows the highest match rate at 87% with a -1.44% average variance against actual sales. This conservative posture reduced offer risk. Both DataTree and Melissa inflated valuations on average compared to RVM.

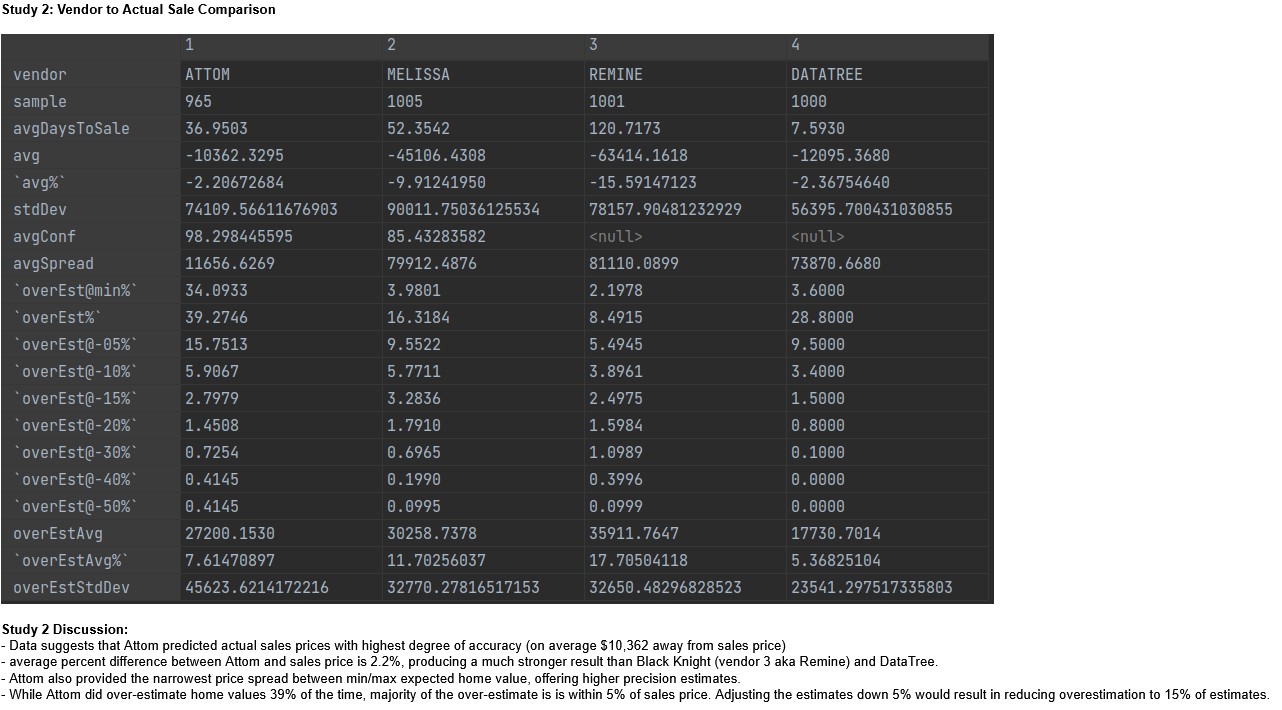

Study 2 — Vendor to Actual Sale Comparison

Four-vendor comparison against actual closed sale prices. Data suggests Attom predicted actual sales prices with the highest degree of accuracy — on average closest to actual sale price — while offering the narrowest price spread between min/max expected home value.

Before & After — Vendor Stack Comparison

| Dimension | Multi-Vendor (Before) | Consolidated Platform (After) |

|---|---|---|

| Vendors | DataTree AVM, Attom Data, Melissa | Attom Bulk Bundle |

| Pricing Model | Per-call - scales with volume | Fixed bulk - no scaling cost |

| Monthly Cost | Significant - three separate contracts | 35% reduction |

| AVM Availability | Varies by vendor | Highest across all three |

| AVM Posture | At or above market value | ~3% conservative - reduces offer risk |

| Departments Served | Siloed - different vendor per function | Unified - marketing, sales, finance |

| Scaling Cost | Increases with every new market | Eliminated |

| Data Freshness | API on-demand | Monthly bulk refresh - centralized DB |

Building the Executive Case

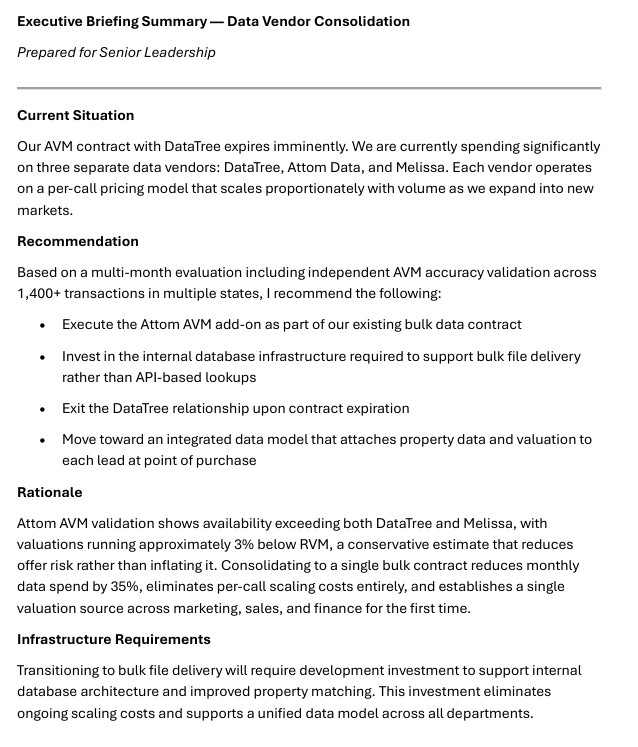

I presented a full briefing to senior leadership which covered the current contract status across all three vendors, the DataTree billing situation, the Attom bundle terms, accuracy validation results, infrastructure requirements, and a clear recommendation to proceed.

Executive Briefing Summary — Data Vendor Consolidation

Executive briefing prepared for senior leadership covering the current situation, recommendation, rationale, and infrastructure requirements. This document drove the consolidation decision.

Redesigning the Infrastructure

The architectural shift was as significant as the vendor decision. The previous model of individual API calls per property lookup across multiple vendors meant data costs scaled with every transaction. The replacement model centralized bulk nationwide data refreshed monthly into an internal database, eliminating per-call costs entirely. While there was a long-term investment required in the platform infrastructure, the data cost savings and operational improvements more than justified the cost.

The Outcome

Monthly data expenditure dropped from 35% with a fixed cost structure that no longer scaled with business volume. More consequentially, the business established unified valuation infrastructure for the first time. Marketing, sales, and finance were working from the same number on every property. The silent inconsistency that had been compounding across every deal was eliminated by design rather than managed by exception.

The Attom AVM's conservative posture also improved underwriting discipline. Offers built on systematically lower valuations reduced the risk of overpaying for assets resulting in a direct improvement to portfolio quality and the credit facility's borrowing base integrity.

What I'd Do Differently

The lesson I took from this experience was about how to frame data infrastructure decisions within a fast-moving organization. Positioning this as back-office cost optimization, even with strong analytical support, meant it competed with feature development and market expansion for resources. In hindsight, leading with the risk to valuation consistency across the credit facility would have prompted a decision more quickly. The lending partners and investors who depended on consistent portfolio valuation would have been a more compelling frame than the cost savings alone. Finance and risk framing moves faster than operational efficiency framing in organizations where capital relationships are central to the business model.